The economic trilemma facing Bayern’s opponents in the Champions League

Reflection on the strengths and weaknesses of various ownership models in European football after Bayern’s victory against Real Madrid

Bayern Munich against Real Madrid, the evergreen classic of European football. But residing in California, I followed my comparative advantage here: watching redwoods. Nonetheless, my team eked out a 4-3 victory (6-4 on aggregate) in stoppage time to advance to the European Champions League (CL) semifinals and make my friends from Madrid unhappy.1 While my dad had to watch Bayern lose the Champions League final in stoppage time in Spain, I had a better time watching Madrid lose a game in a suburb when I was living there.

World-class performance of the Bavarian front three with Premier League roots - Kane, Olise, and Diaz guaranteed Bayern their spot in the final four and more than a hundred million euros of revenues from the CL. The black beast (La Bestia Negra) returned.

But Madrid led three - Mbappé scored the third goal that put Bayern on the edge of defeat. He moved to the old-money stalwarts Real after years of teasing, leaving Parisian oil money behind.

The trilemma of sportive success, financial sustainability, and fan demands

What are the economic forces that make Bayern and Real the leading contenders? Both are shaped by a long tradition that they still benefit from today. The presidents are elected by club members like me. They dominate their national leagues, while being fresher in the deciding games against their richer Northern rivals in Paris and England, who are controlled by oil money from the Gulf or US VC money.

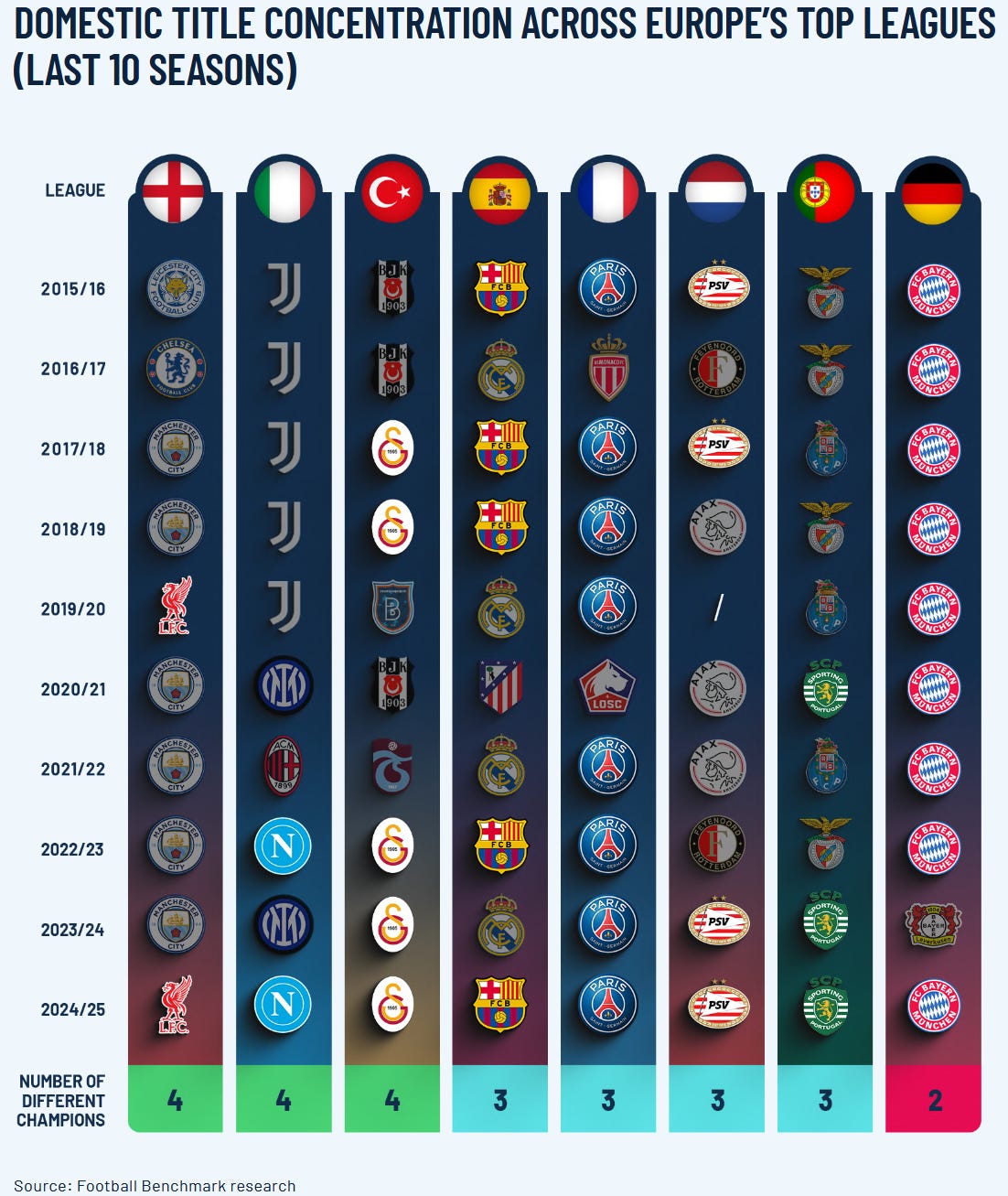

These different traditions and money sources demonstrate the trilemma that European football clubs face. Competitiveness, financial sustainability, and happy fans are three different poles that leagues and clubs have to balance. While oil money clubs serve more prestige than monetary purposes, they aren’t as appealing to fans with reduced matchday atmosphere. Spanish clubs offer cheap season tickets to their members while taking on debt to compete with better-financed rivals. Germany has sacrificed competitiveness on the national level - Bayern has won 9 out of 10 recent championships for providing fans with a good matchday experience and control over their clubs. But the competitors that receive injections of oil money make football competitive with limited margins. So no club achieves a perfect balance between all three. Which pole each club sacrifices depends on who owns it — and there are three broad ownership types dominating the Champions League today.

How each ownership type sacrifices a different pole

But nowadays, the national leagues still dominate most of the game calendar. This also reflects a stronger national than European identity. Three types of ownership forms dominate the Champions League: US private capital (e.g., Liverpool and Chelsea), oil money (PSG and ManCity), and “aristocratic” traditional clubs (Bayern, Real, and Barcelona).2 But all of them have the potential to dominate their national leagues.

First, the only model that keeps profitability somewhat in mind: Venture capital funds. Just like the startups they fund, the upside lies in selling the club more expansively after asset growth, not in making huge profits every year. These clubs are well-run and innovative: Liverpool revolutionized the use of data in any aspect of the game - scouting, training management, and playing style. Visiting the museum at Anfield made me aware of how extraordinarily well the club had performed recently after a long dry spell, thanks to better management from their new US owner, analysis from their data nerds, and coaching from Juergen Klopp. But the model’s failure modes are visible at Manchester United (two decades of extractive dividends under the Glazers while the stadium decayed) and at Chelsea (seven-year contracts as accounting gymnastics, three managers in a season). The sacrifice here is fan access — Premier League ticket prices are the highest in Europe — and often sporting stability at the club level.

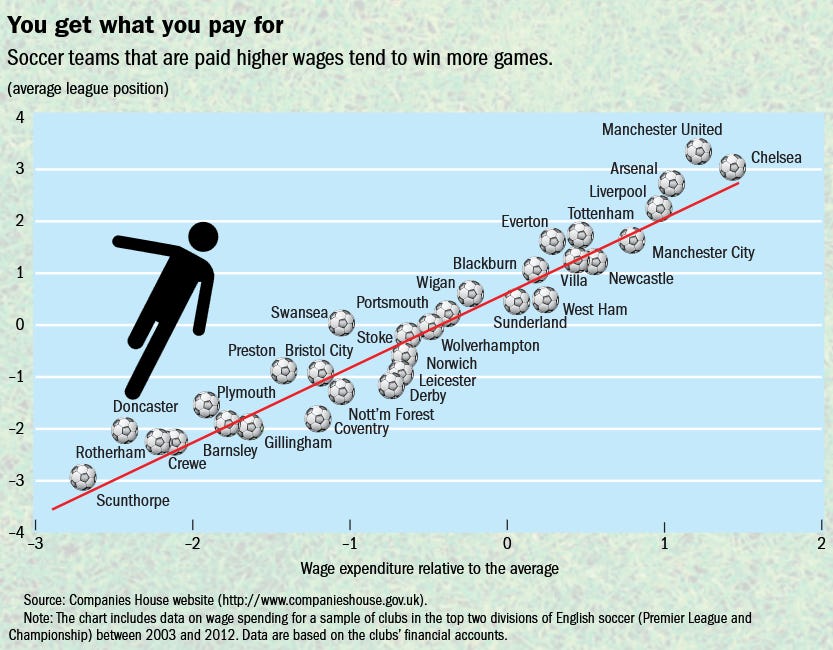

Second, Sheik clubs use football for reputation washing. Unloved by fans, they attract the best players - such as PSG Neymar, Mbappe, and Messi - to attract attention. They regularly face investigations over financial rules. But they can also achieve great success, as ManCity did, winning 6 of the last 8 Premier League titles. They pay higher salaries, which has had moderate success in attracting the best players. They need to pay a higher transfer fee because other clubs are aware of their financial situation. But research shows that in the aggregate, money shoots goals, as higher wage expenditures are associated with more titles.3 During my multiple trips to Paris, I never felt the urge to get to know more about PSG - but this might also be because the outside options for my leisure were good.

Source: Szymanski (2014)

Third, the old-money elite of European football has won the most titles over the decades and offers the greatest allure to players. The top 3 clubs by revenue are Real Madrid, Barcelona, and Bayern Munich. Most clubs have to take on debt to compete with the other types, but some manage to eke out a profit, especially when they dominate their own league, such as Bayern.4 Their museums are filled with silverware, as I experienced in Munich and Madrid.5 While the Spanish clubs retain more broadcast revenue from individual marketing, Bayern6 faces limited international appeal and revenue abroad, whereas English teams generate the most broadcast revenue. But they’re popular brands, as their strength in generating ad revenue demonstrates.

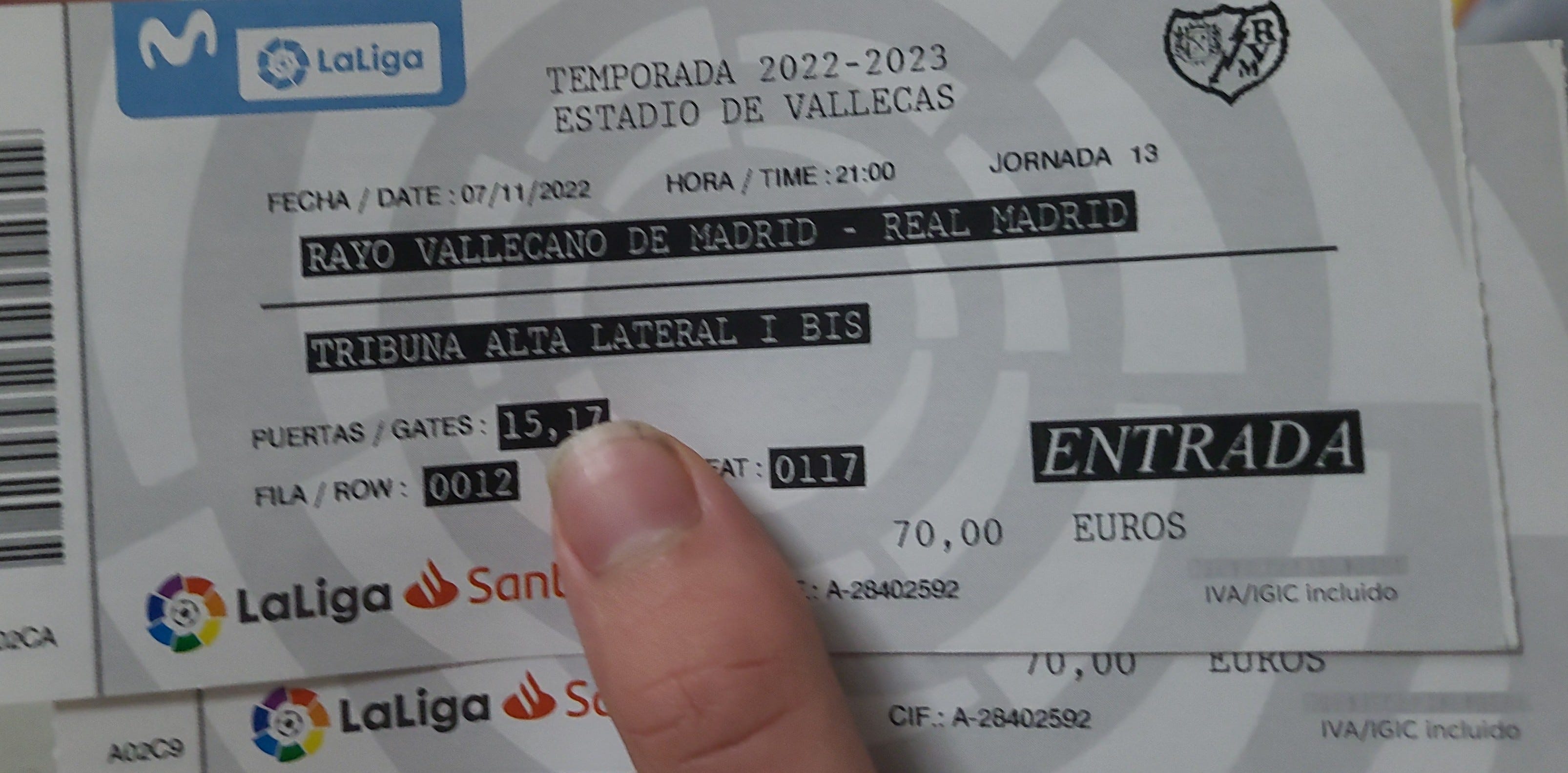

I watched games of all of the Big 3. In Madrid, the tickets were too expensive, so I queued for 3 hours as a poor exchange student to get tickets for the away game in the Vallecas suburb, where they lost for the first time in decades, even after bringing in many world-class players as substitutes.

Away ticket to Rayo Vallecano vs. Real Madrid: three hours queuing to see one of Real’s rare recent defeats in the Madrid area.

Bayern comes closest to balancing all three - profitable, member-owned, and continentally competitive - but at the cost of making the Bundesliga predictable: nine of the last ten titles went to Munich, which is oligopoly, not competition. The 50+1 rule - which guarantees members control over the club - has prevented VCs or Sheiks from taking control of a rival upstart. Ironically, Bayern advocates abolishing it to increase national competition, thereby endangering its national monopoly.

How will economic forces shape the on-pitch performance in the future? The revenue gap between the Premier League and the rest will probably grow. The 70% role could improve profitability if it’s enforced effectively.

Interesting edge cases of this typology are:

Juventus Turin

owned by industrialist family for a century alongside Fiat

traditional dominance of the Italian league

old money

Manchester United

owned by American family that considers selling

are aware ofPrivate capital

historic successes followed by sporting failures while revenue growth continued

Inter Milan

switched owners a lot after a long history

recently US private capital firm received control

Szymanski researches sport economics more general. I received a lot of this insights from reading this book Soccernomics.

Bayern cumulatively made 285 Mio. Euro as profit, while Barcelona was on the brink of collapse after overspending during the late Messi era. FT journalist Kuper describes the downfall packed with petty privileges, wrong reinvesmtnents after the Neymar transfer and a dependence on Messi as reasons in his book.

In Madrid, the president was close to the Champions League trophy in the centre. This central importance of core figures retain most clubs.

Bayern also benefits from the 50+1 rule which most German fans are favoring. This prevents foreign money to gain control in other clubs that could challenge Bayern’s many championships. ironically, Bayern advocates for the abolishment to increase national competition which would endanger their national monopoly.